Managing money isn’t supposed to feel like a monthly brain teaser, right? With so many budgeting apps floating around, picking one can honestly feel like a chore. I’ve gone down the rabbit hole with three of the most popular financial tools, hoping to make your choice a little less stressful.

Each app brings its own flavor to the table: YNAB wants you to rethink spending with zero-based budgeting, Mint keeps things breezy with automatic expense tracking, and Personal Capital leans into investment management while tossing in some basic budgeting. Once you know what each app actually does best, matching it to your goals (and personality) gets a whole lot easier.

The right budgeting app can totally change your relationship with money. But it only works if it fits your actual life. So, let’s dive into features, costs, and what it feels like to use each one—because honestly, you deserve an app that makes money management feel less like a grind.

Key Takeaways

- YNAB is for folks who want to overhaul their spending habits and crave hands-on budgeting.

- Mint is perfect if you want effortless, automated expense tracking.

- Personal Capital is the go-to for investors who want to keep an eye on portfolios while still managing basic expenses.

Core Budgeting Philosophies and Approaches

Every finance app out there has its own budgeting philosophy that shapes how you interact with your cash. Mint leans into automatic tracking and categorization. YNAB wants you to get your hands dirty with “giving every dollar a job.” Personal Capital? It’s all about growing your wealth and tracking investments.

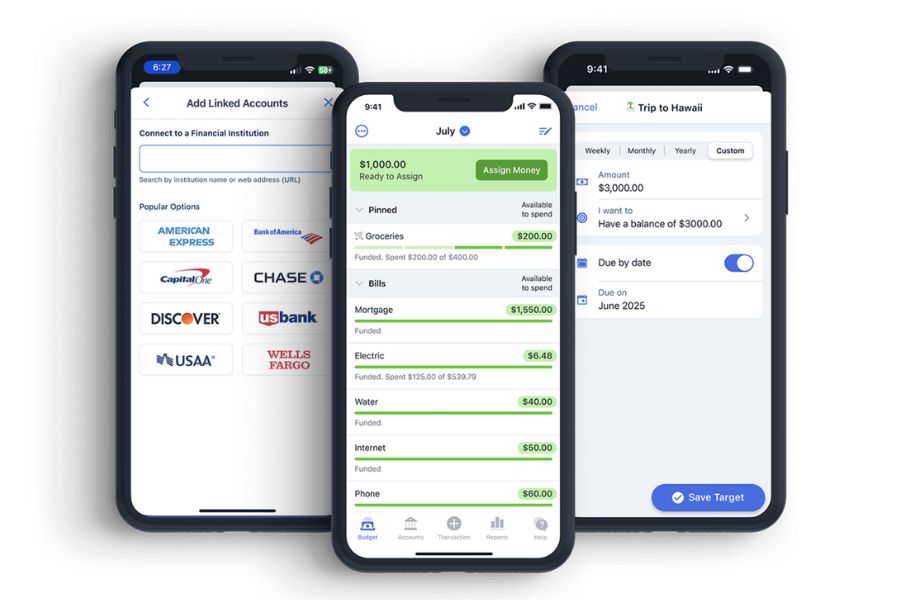

Mint: Passive Financial Tracking

Mint keeps things simple. You link your accounts, and the app sorts your transactions automatically. It then whips up spending reports that show exactly where your money disappears each month.

I’ve noticed Mint feels more like a tracker than a true budget planner. Sure, you can set limits for categories, but it doesn’t make you plan ahead before you spend.

What Mint Does Best:

- Auto-categorizes your transactions

- Breaks down spending with easy reports

- Lets you set budgets (if you want)

- Tracks bills and sends reminders

Mint shines when you want to look back at your spending. Curious about last month’s grocery bill? It’s right there. Wondering if you spent more on takeout this year than last? Mint shows you.

If you’d rather watch your finances than actively manage every penny, Mint’s your friend. It won’t nag you to change your habits—it just lays out the facts.

YNAB: Proactive Budgeting and Methodology

YNAB flips the script with its “give every dollar a job” mantra. Before you spend, you assign every dollar to a category.

It makes you get intentional with money. You literally can’t spend what you haven’t budgeted, which keeps overspending in check and nudges you toward better decisions.

YNAB’s Four Rules:

- Give every dollar a job

- Embrace your true expenses

- Roll with the punches

- Age your money

I’ll be honest—YNAB takes some getting used to. You need to check in often, tweak categories, and move money around as life happens.

But it’s not just about today’s bills. YNAB wants you to plan for the big stuff—car repairs, holidays, surprise vet visits—by saving a little each month. That way, you’re not blindsided.

If you’re ready to really change your money habits and don’t mind a bit of effort, YNAB is a game-changer.

Personal Capital: Wealth and Investment Focus

Personal Capital approaches money from the angle of building wealth. It’s not so much about daily budgeting—it’s about seeing the big picture with investments and net worth.

Honestly, Personal Capital’s budgeting tools feel basic next to Mint or YNAB. Yes, it sorts your transactions and shows trends, but it doesn’t let you dig deep into budgets.

Where Personal Capital Excels:

- Tracks your investment portfolio

- Calculates your net worth

- Analyzes investment fees

- Offers retirement planning tools

Personal Capital gives you a bird’s-eye view of your finances. You can see all your investment accounts in one spot and analyze how your portfolio is really doing.

It’s designed for folks who already have their spending under control and want to focus on growing their net worth. If you’re more about optimizing investments than tracking every latte, this one’s for you.

Detailed Features Comparison

Each app brings a unique spin to money management. YNAB is all about hands-on budgeting. Mint automates tracking for free. Personal Capital zeroes in on investments and net worth.

Account Linking and Setup Experience

YNAB asks you to set up accounts manually at first, though you can now sync banks. It’s a bit of a process, but you get total control over budget categories. The learning curve is real, but the 34-day free trial gives you time to adjust.

Mint makes setup a breeze. It connects to banks, credit cards, and loans in minutes. The setup wizard guides you, and everything syncs with barely any effort.

Personal Capital wants to know about your investment and banking accounts right away. It connects to over 20,000 institutions and asks about your financial goals to personalize things.

Budgeting and Money Management Tools

YNAB uses zero-based budgeting—every dollar gets assigned a job. You move money between categories as needed. It’s hands-on and builds solid habits, but you’ll need to check in daily.

Mint auto-creates budgets based on your spending. It tracks expenses and sends alerts if you go over. The budgeting runs quietly in the background.

Personal Capital keeps budgeting simple. It tracks expenses and shows trends, but the tools are basic compared to the other two.

Financial Goals and Savings Tracking

YNAB treats savings goals like any other budget category. You assign cash to each goal every month until you hit your target. This approach ties savings directly to your budget.

Mint tracks savings goals separately from your budget. It monitors your progress and estimates how long you’ll need to reach each goal at your current savings rate.

Personal Capital offers goal planning for retirement and big purchases. It uses your investments and income to see if you’re on track. The tools feel more advanced for long-term planning.

Investment and Net Worth Monitoring

YNAB sticks to budgeting. If you want to track investments, you’ll need another app.

Mint offers basic investment tracking and net worth calculations. It shows your portfolio balance and an overall snapshot, but nothing too deep.

Personal Capital leads the pack here. You get detailed analysis—asset allocation, performance metrics, fee breakdowns, and daily net worth updates.

Security, Privacy, and Data Protection

All three apps use bank-level encryption to keep your data safe. They each offer two-factor authentication and stick to strict security standards.

Authentication Methods

YNAB and Mint both offer two-factor authentication for extra protection. You get a second step beyond just your password.

Both support biometric login on your phone—Touch ID, Face ID, or fingerprint. It’s quick and secure.

The apps make you re-enter your credentials if you jump between them. That way, nobody can snoop if they grab your unlocked phone.

Mint, owned by Intuit, follows the same security playbook as TurboTax and QuickBooks. Personal Capital matches that with similar authentication options.

Encryption Standards and User Data Safety

All three use bank-level encryption or better. Your login info stays encrypted—no one at these companies can see your actual passwords.

They create secure connections with your banks, so your data updates automatically without exposing sensitive details.

YNAB and Mint encrypt data in transit and at rest. Personal Capital follows the same playbook to keep your investment and banking info locked down.

Pricing and Subscription Models

Each app approaches pricing differently. Mint is totally free, YNAB charges a monthly fee, and Personal Capital gives you free basics with paid premium options.

Free vs Paid: What You Get

Mint stands out as a free budgeting app. You get full access to budget tracking, bill reminders, and credit score monitoring. They make money through ads and partner offers.

YNAB charges a subscription for advanced budgeting, goal tracking, and detailed reports. It’s about teaching you to budget, not just track.

Personal Capital offers a free tier for investment and net worth tracking. Paid services include financial advice, but those start at higher balances and fees.

So, Mint gives you everything for free. YNAB makes you pay for the full toolkit. Personal Capital gives you investment tracking for free, with add-ons if you want advice.

Subscription Fees and Free Trials

YNAB runs $14.99 a month or $109 a year (if you pay annually). You get a 34-day free trial to try everything before deciding.

Personal Capital’s free version covers most needs. If you want their advisory services, you’ll need at least $100,000 in assets and will pay about 0.89% a year.

Mint never charges. No hidden fees, no premium upgrades—just ads.

Reporting, Alerts, and User Experience

Each app handles reports and notifications differently. Mint gives you the big financial picture and credit monitoring. YNAB focuses on budget alerts. Personal Capital is all about investment analytics.

Spending Reports and Insightful Analytics

Mint gives the most complete overview. You get detailed spending reports by category, month, and merchant. It tracks your credit score automatically and shows trends.

It also connects to your loans—mortgage, car, student loans—so you can see balances and payment schedules.

YNAB zooms in on your budget. Reports show how well you stuck to categories, where you overspent, and where you saved.

Personal Capital shines for investments. You see net worth, asset allocation, and portfolio performance. The retirement planner includes a loan calculator for big purchases.

The fee analyzer is a hidden gem—it shows you what you’re paying in fund expenses. I switched to lower-cost funds after seeing the numbers.

Real-Time Alerts and Notifications

Mint sends alerts for bills, unusual spending, and low balances. You can set custom alerts for categories like dining or shopping.

Credit score monitoring alerts let you know if your score changes or there’s suspicious activity.

YNAB’s alerts are all about your budget. You’ll get pinged when you’re close to maxing out a category or need to enter transactions.

Personal Capital sends fewer alerts. Mostly, you’ll get notified about big transactions or monthly summaries. The focus is on investment changes, not daily spending.

Choosing the Right Financial App for Your Needs

The best budgeting app really depends on how you manage money and what you want to achieve. Your habits and style should drive your choice.

Aligning App Features with Financial Habits

I’ve noticed that your daily habits matter more than you think. If you check your accounts all the time, Mint is great—it pulls in your data automatically.

Hands-off? Mint keeps things updated with almost zero effort. You’ll see where your money goes without logging every coffee run.

Detail-oriented? YNAB makes you plan every dollar before spending. It’s perfect if you want to break bad habits and get proactive.

Personal Capital fits if you’re focused on long-term wealth. It tracks net worth and investments better than the others.

Active spenders who are always on the move will appreciate YNAB’s mobile app for entering transactions right away.

Passive trackers will love Mint’s automatic updates and timely alerts.

Factors to Consider for Different Budgeting Styles

Let’s be honest—your budgeting style makes or breaks your relationship with money apps. If you want real results, you’ve got to match the right tool to how you actually think about spending.

Zero-based budgeters? Go with YNAB. It’s the only app I’ve tried that forces you to assign every dollar a job before you spend it. No wiggle room, but that’s kind of the point.

Envelope method fans—YNAB’s category setup nails it for you, too.

Set-it-and-forget-it types? Mint’s your friend. It tracks spending automatically, so you don’t have to poke at it every day. I’ve used it when life got busy, and honestly, sometimes you just want something easy.

Here’s a quick cheat sheet:

| Budgeting Style | Best App | Key Reason |

|---|---|---|

| Zero-based | YNAB | Forces dollar assignments |

| Automatic | Mint | Minimal user input needed |

| Investment-focused | Personal Capital | Tracks portfolio performance |

If you’re new to budgeting, Mint feels less overwhelming. It just runs in the background and lets you see where your money’s going.

But if you crave strict control, YNAB’s hands-on method gives you that power. I know people who swear by it for that reason alone.

Got unpredictable income? YNAB really shines here. It helps you plan ahead in a way that other apps just don’t.

Frequently Asked Questions

People always want to know how Mint, YNAB, and Personal Capital stack up in real life. I’ve seen these questions come up over and over, so let’s tackle them head-on.

What are the top features that set Mint, YNAB, and Personal Capital apart in financial management?

Mint? It’s all about automation. The app connects to your bank, sorts transactions, and reminds you about bills—no heavy lifting required. Plus, it’s free and even shows your credit score.

YNAB works differently. You give every dollar a job before you spend it. This zero-based approach really helps if you’re trying to break bad spending habits or save more.

Personal Capital is the investment nerd’s dream. It breaks down your portfolio, tracks your net worth, and offers retirement planning tools. If you love charts and projections, this one’s for you.

How do YNAB’s budgeting capabilities compare to those of Personal Capital and Monarch Money?

YNAB makes you plan for every purchase. You assign funds to categories, tweak as life happens, and get more mindful about spending. It’s a bit of work, but the payoff is real.

Personal Capital leans into tracking, not budgeting. You see where your money flows, but it doesn’t push you to make spending decisions. Its budgeting tools are pretty basic.

Monarch Money lands somewhere in the middle. It auto-categorizes like Mint, but lets you customize things more. If you want something between hands-on and hands-off, Monarch’s worth a look.

Can you find premium budgeting tools in any free budget apps that compete with Mint or YNAB?

Mint packs a lot in for zero dollars. You get automatic categorization, bill tracking, credit score updates, and some investment tracking. Honestly, I haven’t seen another free app that matches all of that.

YNAB isn’t free, but you can try it out before paying. Some banks and credit unions also offer free zero-based budgeting tools to their members, so check with yours.

Personal Capital gives you net worth tracking and basic investment analysis for free. If you want the advanced stuff, though, you’ll need to pay.

What financial app does experts like Dave Ramsey recommend for effective budgeting and why?

Dave Ramsey actually built his own app—EveryDollar. It’s zero-based, just like YNAB. He says this method forces you to get intentional with your money, and honestly, he’s not wrong.

A lot of experts recommend YNAB for folks who struggle with overspending. The hands-on approach helps you build better habits over time.

If you’re just starting out, Mint is a popular pick. It’s low effort and helps you see your spending patterns before you dive deeper.

Is Personal Capital the best tool for investment tracking compared to Mint and YNAB?

Personal Capital really stands out for investment tracking. It breaks down your portfolio allocation, fees, performance, and even retirement projections. That’s its main superpower.

Mint gives you basic investment tracking for free. You’ll see your balances and some performance data, which is fine for simple needs.

YNAB sticks to budgeting. It’ll show account balances, but if you want investment analysis or advice, you’ll need to look elsewhere.

Considering user satisfaction, which app ranks highest among Mint, YNAB, and Personal Capital?

Let’s dive right in—when it comes to actually changing how people handle money, YNAB (You Need a Budget) takes the crown. I’ve seen folks rave about how it helps them finally get control, not just track numbers.

Mint’s a favorite for anyone who wants a free, hands-off experience. The automatic syncing is super convenient. But honestly, the ads can get on your nerves, and sometimes the data’s a bit off.

Personal Capital attracts users with its investment tracking tools, which are pretty slick if you’re into growing your portfolio. That said, those persistent sales calls? Not everyone’s a fan. The free version gets solid praise, but opinions about the paid service are all over the place.